Pursuant to Section 21(2)(c) of Act No. 23/2017 Coll. on the Rules of Budgetary Responsibility (hereinafter “Act”), the Czech Fiscal Council (CFC) monitors general government finances. As part of this activity, it also seeks to identify risks that may negatively affect the stability of public finances in the short, medium and long term. Since September 2018, the CFC has been informing the public about its conclusions on a quarterly basis.

Initial economic situation

Gross domestic product (GDP) grew by more than 2% year-on-year (y-o-y) for the fifth consecutive quarter (specifically by 2.2% in the first quarter of this year). Growth was driven exclusively by domestic demand. Household consumption rose by 3.4%, and gross fixed capital formation by 7.3%. Net exports made a negative contribution, due to an 8.2% y-o-y increase in imports. Quarter-on-quarter (q-o-q) GDP growth of 0.2% showed a similar structure as it was driven by household consumption (by 0.6%) and gross fixed capital formation (by 2.0%). Net exports had a negative impact, and government consumption also fell (-0.3%) as a result of the provisional budget. However, economic growth in the first quarter was weaker than expected, which poses a potential risk to achieving 2% economic growth in 2026, as the economy would need to grow by an average of 0.5% q-o-q over the next three quarters of the year.

The y-o-y inflation rate stood at 2.5% in April but fell to 2.1% in May. Although the growth in prices is being driven up by fuel prices, these have not yet been passed on to other categories. Any pass-through of higher fuel prices to end-user prices is not expected to affect inflation until the second half of the year. From the perspective of next year’s state budget, the inflation rate in June is crucial, as this feeds into the pension indexation scheme in the form of so-called pensioner inflation.

Wages and salaries continue to show strong growth, with their nominal volume rising by 8.9% y-o-y in the first quarter. The average wage rose by 6.4% in real terms. The general unemployment rate has stabilised, reaching 3.2% in April for the eighth consecutive month and remaining one of the lowest rates in the EU.

General government finances and fiscal policy settings for the coming years

At the end of May, the state budget recorded a cash deficit of CZK 170.2 billion, or CZK 190.0 billion after adjusting for timing differences in revenue and expenditure relating to EU projects. The expenditure side of the state budget is currently developing in line with the expectation. However, it is still largely influenced by the provisional budget in the first quarter of the year, and a number of non-mandatory expenditures will be carried over to the second half of the year. For example, non-investment transfers to public universities are down by CZK 13.7 billion y-o-y, and their uptake is expected in the coming months. Conversely, for payments for state-insured persons (healthcare), the volume of funds disbursed is CZK 14.9 billion higher y-o-y, which is influenced by an advance payment of CZK 13.1 billion. Investment purchases are also higher y-o-y (by CZK 9.3 billion), which is mainly related to the procurement of military equipment by the Ministry of Defence (CZK 6.1 billion) and the acquisition of a new building for the Financial Administration of the Czech Republic (CZK 2.0 billion).

State budget revenue reflects the aforementioned strong wage growth and the associated rise in household consumption. At national level, y-o-y revenues of personal income tax paid by taxpayers rose by 11.8%, value added tax by 8.6% and social security contributions by 6.5%. Corporate income tax is also performing well, with collections currently rising by 17.4%. Excise duty on mineral oils has so far increased by 7.1% y-o-y, driven by continued solid economic growth, which is also reflected in transport activity. Given the timing of this tax’s due date, the decline in revenue resulting from the waiver of part of the excise duty, effective from 8 April, will only become apparent later. The excise duty waiver has a fiscal impact of approximately CZK -1 billion per month, and if this waiver continues to the same extent at least until mid-September, the revenue shortfall of approximately CZK 5 billion will already be classified as a one-off measure.[1]

At the end of April, local government sector had a cash surplus of CZK 31.1 billion, which was the result of the financial performance of the regions (CZK +27.0 billion) and the City of Prague (CZK +9.2 billion). Conversely, municipal budgets were, surprisingly for this time of year, in deficit at the end of April (CZK -5.4 billion), which may indicate deeper structural changes in their behaviour. The CFC is paying, and will continue to pay, close attention to this phenomenon.[2] The Ministry of Finance’s (MoF) May forecast revises local government surpluses for the years 2026 to 2029 down to 0.4% of GDP from the previously commonly achieved level of 0.7% of GDP. Health insurance companies had a cash surplus of CZK 9.7 billion at the end of April but without the advance payment for state-insured persons amounting to CZK 13.1 billion (see above), the cash balance would have been CZK -3.4 billion. The public health insurance system is projected to run a deficit of CZK 15.0 billion in 2026, and considering the increase in overdue liabilities, the accrual deficit will reach approximately CZK 19 billion.[3]

According to the MoF, the general government deficit is expected to reach 2.6% of GDP this year, which was the figure anticipated and communicated by the CFC in its previous opinion[4]. In 2027, the CFC expects a deficit of around 3% of GDP; however, the final figure will depend critically on any further discretionary measures adopted by the government on both the revenue and expenditure sides of the state budget regarding its approval. The deficit for 2027 has also been revised in the Czech National Bank’s forecast (from 2.7% to 3.1% of GDP), and the European Commission (EC) expects a similar figure for 2027 in its May forecast (2.9% of GDP).

The CFC also points out that, as a result of changes to the Czech fiscal rules (see below), the entire budgetary process has been postponed until August, and April (including this year) is no longer a key date for setting the binding state budget balance for the following year. Although the government has approved the so-called Budgetary Strategy for 2027 and 2029, which implies a maximum cash deficit in 2027 (including repayable financial assistance for the construction of the Dukovany nuclear power plant) of CZK 190 billion,[5] the government is negotiating a new fiscal-structural plan with the EC (see below)[6], the draft of which anticipates a significantly higher balance.

This also disrupts the existing logical structure based on setting a maximum “expenditure ceiling” in April, followed by political decision-making on the allocation of expenditure during the summer and the approval of the final budget in August. That is also why no definitive ceiling for the state budget deficit is currently being worked with, but only an estimate. Based on data available as of today, the CFC calculates that, provided the 3% Maastricht criterion is met, the state budget deficit for next year may exceed CZK 350 billion[7] . The state budget balance itself (without necessarily affecting the general government balance) is likely to be influenced next year by a significant increase in payments for state-insured persons of approximately CZK 24 billion[8]. This amount significantly exceeds the standard increase according to the indexation formula, which is expected to have an impact of around CZK 3 billion on the state budget next year.

Following discussions with representatives of the EC, the MoF has drawn up a draft of the new fiscal-structural plan for the period 2027 to 2030 (FSP). The draft is due to be submitted to the government for approval by 15 June, and final approval from the EC is expected by the end of July.

The previous FSP (approved for the years 2025 to 2028) was based on technical information from the EC, which required the achievement of a primary structural surplus of 0.4% of GDP in 2028. The new requirement is to achieve a primary structural surplus of 0.5% of GDP in 2030 (the draft includes 0.3% of GDP due to different macroeconomic assumptions of MoF compared to the EC). In any case, from a medium-term perspective, the new plan reflects the previous one and the target does not change significantly.

The new plan confirms the desired consolidation but postpones it and concentrates it in 2028 and 2029, i.e. up to the year of the regular elections to the Chamber of Deputies of the Parliament of the Czech Republic. Conversely, in 2027, it loosens fiscal policy and, according to the CFC’s interpretation, even allows the general government deficit to exceed 3% of GDP, although it implies a balance of only -2.8% of GDP. The MoF adds that “the fiscal framework respects the government’s targets not to exceed the 3% of GDP deficit limit for the general government sector. Should such an overshoot nevertheless occur, it should be covered by the application of the defence escape clause.” The CFC points out that the structure of the European defence escape clause allows the Czech government to exceed the set balance by approximately 0.3 to 0.4% of GDP even with defence expenditure below 2% of GDP.

The CFC considers it important to draw attention to the amendments to the acts that will change the national fiscal rules by relaxing them to an unprecedented extent, meaning that any government will be bound only by fiscal rules at European Union level. The purpose of national fiscal rules lies primarily in ensuring that Czech public finances remain within a range that will sufficiently protect them from breaching EU rules, or rather, before financial markets begin to effectively enforce the long-term sustainability of Czech public finances.

The CFC considers the following to be key changes to national fiscal rules:

- The introduction of a new exemption from the expenditure ceilings of the state budget and state funds, which is to apply to the infrastructure projects. The exemption has no quantitative limit, but only a time limit, namely for the years 2026 to 2036. The exemption from expenditure limits is to apply to the projects listed in the annex to Act No. 416/2009 Coll., on the Acceleration of the Construction of Strategically Important Infrastructure (the so-called ‘Linear Act’), which covers a very broad range of projects whose total cost cannot currently be reasonably calculated.[9]

- Extension of the existing exemption from the expenditure limits of the state budget and state funds for defence expenditure, specifically until 2036 instead of the original 2033. This is an exemption whereby defence expenditure exceeding 2% of GDP is not counted towards expenditure limits, and the CFC expressed doubts[10] as early as the first year of its application as to whether it was being applied in accordance with its intended purpose.

- Allowing state budget expenditure to be increased by up to 10% in the event of a “deterioration in the security situation, particularly in connection with the fulfilment of obligations arising from Article 4 or 5 of the North Atlantic Treaty”. According to the CFC, this is a provision that disproportionately increases the government’s budgetary leeway, as it will not require the consent of the Chamber of Deputies of the Czech Republic for such an increase in budgetary expenditure, and as the provision does not clearly and exhaustively specify under what circumstances budgetary expenditure may be increased to that extent.

- At the same time, the CFC notes that it remains unclear whether, in the event that the government’s draft state budget bill is returned to the government by the Chamber of Deputies of the Czech Republic for revision, the restrictions on the government arising from the legally defined maximum expenditure frameworks apply or not. The amendments tabled regarding the set of changes to fiscal rules in the Chamber of Deputies have not yet resolved this issue, which is key for the CFC. The CFC believes in the intend of the MoF to clarify this matter, though this requires the approval of the tabled amendment to another piece of legislation, specifically the changes to the Rules of Procedure of the Chamber of Deputies.

As of the date of this opinion, the aforementioned changes have been approved at the third reading of the relevant acts in the Chamber of Deputies of the Czech Republic and are currently being debated in the Senate. Should they be approved, the Czech Republic will find itself in a situation where national fiscal constraints will essentially cease to exist. The CFC views the amendments to budgetary legislation as a shift in the fiscal paradigm and a departure from the declared (and incorporated into the still-valid wording of the Act on Budgetary Responsibility) reduction of structural public budget deficits to 1.25% of GDP in 2027 and 1.00% of GDP from 2028 onwards (prior to any potential use of the defence exemption).

The CFC also points out that the yield on 10-year government bonds is currently approaching the 5% mark, i.e. a level that has historically been reached mainly during periods of exceptional financial and geopolitical turmoil. Higher long-term interest rates imply higher public debt servicing costs, and their higher level will increase interest expenditure in the state budget and further restrict fiscal space. Interest costs are expected to rise to as much as 1.6% of GDP in the coming years, a consequence of refinancing existing debt and issuing new debt during a period of significantly higher interest rates compared to the past. In this context, the CFC points out that the Czech Republic will also finance its planned investment expenditure at costs that will imply significantly higher debt servicing costs in the future. This makes it all the more important to weigh up not only how much investment expenditure to finance, but also which of these projects actually meet the criteria for classification as investment expenditure in an economic, rather than merely an accounting, sense. The CFC will subsequently publish analyses and opinions on this absolutely crucial topic of public finance.

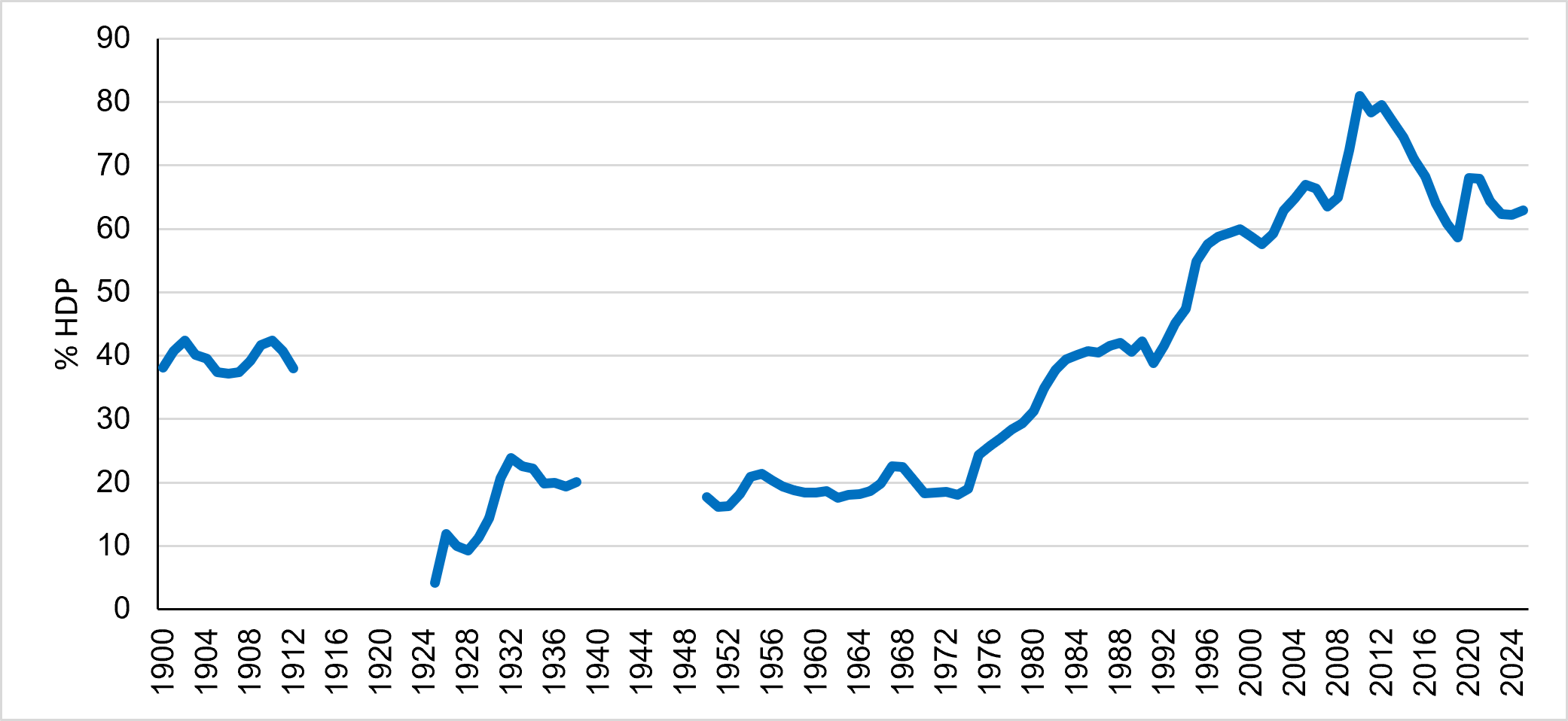

Last but not least, the CFC is monitoring the current debates on the topic of debt – investment – economic growth. However, even in the past, periods of significant economic growth mentioned in this context were not linked to a prior or concurrent increase in public debt. For example, Germany’s debt-to-GDP ratio during the so-called economic miracle (1948 to 1966) remained stable and low, and until German reunification in 1990 did not exceed the level that the Czech Republic is already reaching. Nor was the general government balance significantly in deficit; on the contrary, in some years it was in surplus. The narrative of debt creation (an increase in the debt-to-GDP ratio), followed by economic growth and the repayment of debt through growth (a reduction in the debt-to-GDP ratio), is not supported by the data. Figure 1 shows the development of Germany’s public debt-to-GDP ratio during the 20th and 21st centuries.

Figure 1 : Germany’s general government debt as a percentage of GDP, 1900–2025

Data: IMF (2026), in periods where the graph is interrupted, the necessary data is not available according to the IMF

[1] According to common methodology of the Ministry of Finance (MoF) and CFC, only the measures exceeding 0.05% of GDP are classified as one-off measures. In 2026, this amounts to approximately CZK 4.5 billion.

[2] CFC blog, article by L. Komárek and R. Kalabiška: Prague in the plus, others in the minus: What is happening to their funds? [available in Czech only].

[3] Ministry of Health document: Assessment of the Projected Development of the Public Health Insurance System Based on Health Insurance Companies’ Draft Health Insurance Plans for 2026.

[4] CFC Opinion No. 1/2026: on the development of general government finances and fiscal and budgetary policy

[5] Budgetary strategy for 2027–2029 [available in Czech only].

[6] Press release from the MoF (8 June 2026): The Czech Republic is closer to a new fiscal-structural plan [available in Czech only].

[7] When recording repayable financial assistance for the construction of the Dukovany II nuclear power plant in the cash balance in accordance with current legislation.

[8] This amount is set out in the government-approved draft bill amending Act No. 592/1992 Coll., on Public Health Insurance Contributions.

[9] Such projects currently include, for example, the Týniště nad Orlicí – Častolovice – Solnice and Otrokovice – Vizovice railway lines, or the Líbeznice – Mělník – Česká Lípa Class I road.

[10] Statement of the CFC: the current and expected work on the state budget for 2026, the process of its preparation and the outlook for public finances in the coming years